Truist Financial Corporation has recently launched its initial Open Banking integration, linking up with Mastercard’s Open Finance platform via APIs.

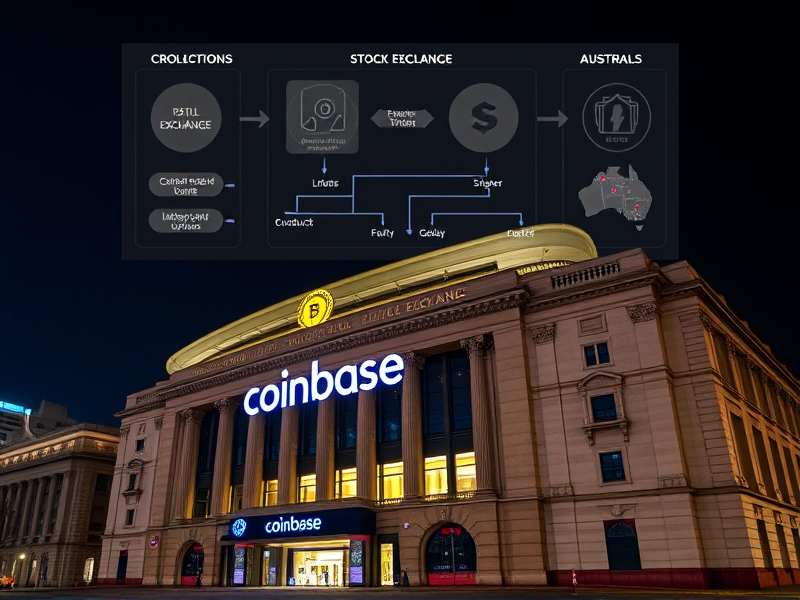

Following the announcement, Truist Financial Corporation introduced an API-driven Open Banking platform as its first direct connection to a financial technology network. This early integration uses Mastercard’s Open Finance technology, providing centralized access to consumer and small business clients’ financial data through various fintech applications.

The platform enables clients to authorize which applications can access their financial data and for what purposes, employing tokenized connections that eliminate the need to share usernames or passwords. This method aligns with broader industry efforts to shift away from credential-based data sharing, which has long been viewed as a security risk in Open Banking environments.

Tokenized Access and Data Control

According to the official press release, Truist clients can now authorize or revoke access to their financial data directly through the integration, allowing seamless connection with fintech tools of their choice via Mastercard’s API connectivity layer. The platform is designed to support use cases like payment initiation, financial health monitoring, and credit product access for those with limited credit histories.

While Open Banking in the US has progressed more slowly compared to markets such as the UK and EU, where regulatory frameworks such as PSD2 have driven standardized API adoption since 2018, the Consumer Financial Protection Bureau (CFPB) finalized its Open Banking rule under Section 1033 of the Dodd-Frank Act late last year. This rule establishes consumer data rights and compliance timelines for financial institutions. Truist’s move indicates growing momentum among US banks to develop compliant direct API infrastructures in anticipation of these deadlines.

Mastercard’s Open Finance platform operates across multiple markets, acting as a connectivity layer between financial institutions and third-party providers. By choosing Mastercard as its first integration partner, Truist gains access to an extensive network of fintech applications without the need for independent bilateral connections.

The platform is accessible to both retail consumers and small business clients, a segment where Open Banking adoption has traditionally been slower than consumer banking. Small businesses can benefit from use cases such as automated cash flow visibility, simplified account aggregation, and access to alternative credit assessment tools that rely on transaction history rather than traditional credit scores.

The launch places Truist alongside other US financial institutions building direct API frameworks in anticipation of broader Open Banking adoption. As the CFPB rule gradually imposes requirements based on institution size, these direct integrations are likely to become a standard expectation rather than a competitive differentiator.