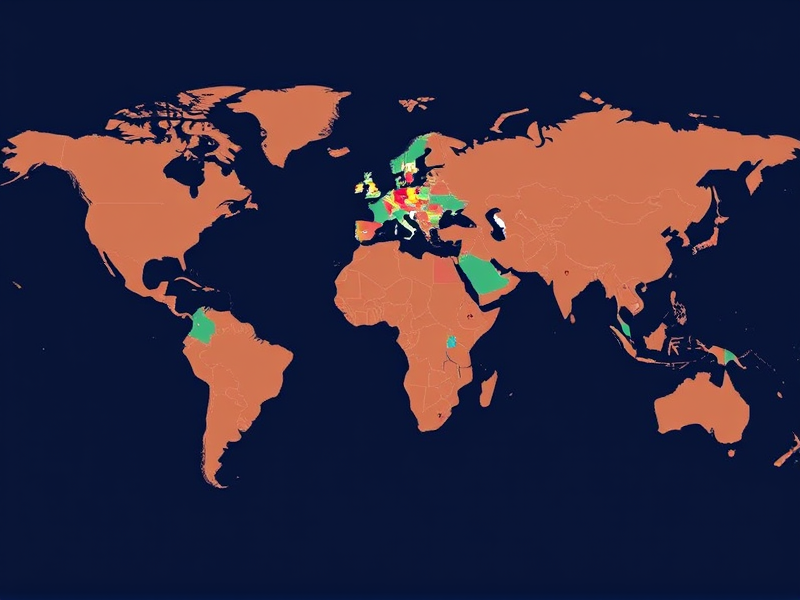

Socure has broadened its bank account verification solution to serve over 30 countries beyond the United States and Canada.

In line with this development, Socure, a US-based company that offers identity and risk decisioning services, has expanded its Bank Account Verification capabilities internationally. The enhancement now allows businesses to verify bank accounts in real time for various purposes such as cross-border payments, global payroll management, marketplace disbursements, lending activities, refund processes, person-to-person (P2P) transfers, and person-to-account (P2A) transactions.

This new solution is integrated into Socure’s RiskOS platform and does not necessitate user logins or redirects. According to the company, it provides up to 98% coverage for account status checks and up to 82% ownership verification, with decision-making typically completed within two seconds upon submission of a name, routing number, and account number.

Regulatory landscape and market needs

The expansion is timely as Nacha plans to enforce updated Automated Clearing House (ACH) rules starting March 20, 2026. These updates emphasize the need for robust fraud monitoring mechanisms that go beyond mere confirmation of account status. Both originators and recipients are expected to implement commercially reasonable measures to prevent unauthorized transactions and fraudulent activities.

Current account validation methods often rely on user-permitted logins or manual micro-deposits, which can verify the existence of an account but fail to validate ownership and authenticity. These tools typically operate within closed banking systems, restricting comprehensive visibility across a wide range of financial institutions.

In contrast, Socure’s approach unifies account status and ownership validation with integrated fraud intelligence, encompassing identity verification, device signals, and first-party fraud indicators in one automated process. This solution caters to neobanks, fintechs, credit unions, payment providers, and international financial institutions beyond traditional banking ecosystems.

Organizations that adopt this technology can preemptively detect suspicious funding activities in sectors like deposits, remittances, gaming, and brokerage accounts. This proactive approach helps minimize ACH return issues due to insufficient funds or unauthorized claims, as well as mitigates losses from misdirected payments resulting from account takeovers. Implementation is reported to be straightforward, with flexible verification steps available when higher risk levels are detected.

The international launch positions Socure to meet the rising demand for fraud-conscious, real-time payment systems in regions where cross-border transactions and global payroll services are becoming more prevalent amid stricter regulatory oversight.