Google Pay has launched a feature called Pocket Money within India’s UPI Circle infrastructure, enabling primary account holders to grant limited transactional access to secondary users like children or dependents without requiring them to have their own bank accounts. This feature repositions the platform as an instrument for organized household financial management beyond its traditional peer-to-peer and merchant payment functionalities.

Two Modes of Delegation

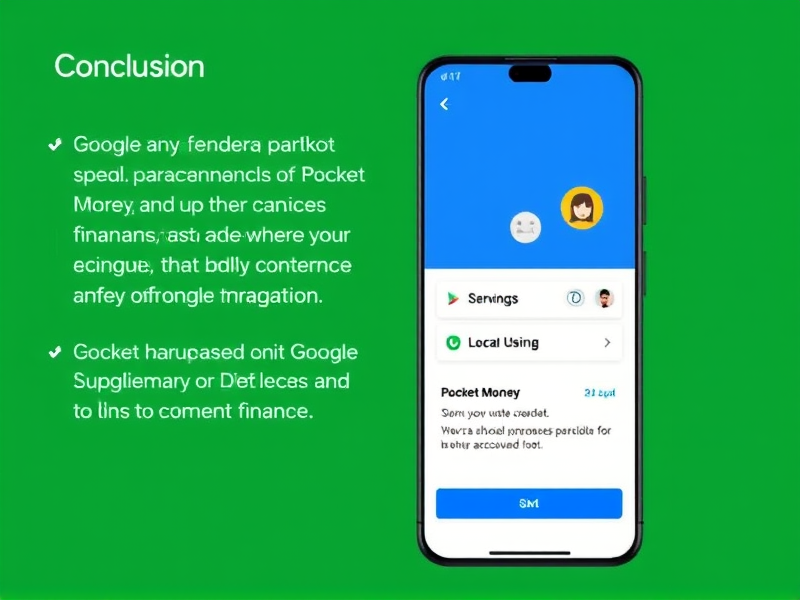

Pocket Money functions through two unique control setups. In one mode, the primary account holder sets a monthly spending limit for the secondary user (reported to be up to INR 180) allowing them to make purchases freely without needing individual approval. In the other setup, every transaction by the secondary user requires real-time authorization from the primary account holder before any funds are deducted, providing greater oversight.

Once added to a UPI Circle, secondary users can scan QR codes, make merchant payments, and send transfers on UPI-supported platforms. The primary account holder receives immediate notifications, ensuring ongoing awareness of spending activities regardless of the chosen mode. This setup mirrors traditional allowance systems but operates in a fully digital and transparent environment.

Implications for India’s Payments Ecosystem

The launch underscores a transition within consumer payment platforms in India, where UPI has become the primary retail payment method. Google Pay’s introduction of controlled access reflects an effort to address a growing number of younger users who frequently engage with digital payments but lack independent banking relationships. By integrating into the existing UPI Circle framework established by NPCI, this feature operates within a defined regulatory context rather than introducing new structures.

For the broader ecosystem, this development highlights that established UPI platforms are broadening their focus from mere transactional utilities to encompassing tools for household financial management. Supervised spending features like these could have significant implications for financial inclusion, particularly among teenagers and young adults who are building familiarity with formal financial systems. The success of similar features on competing UPI applications remains uncertain, but Google Pay’s implementation establishes a clear benchmark in the market.