FedNow Expansion

FedNow, adopted by over 1,600 U.S. financial institutions, has seen significant growth in transaction volume and value since its launch two years ago. Yet, a key limitation remains: participants are restricted to using Reserve Banks as intermediaries for cross-border transactions.

This constraint hinders the utilization of FedNow for international payments, despite its potential for streamlining domestic transfers. Recognizing this gap, the U.S. Federal Reserve is considering lifting these restrictions, bringing FedNow closer to the functionality of established systems like Fedwire.

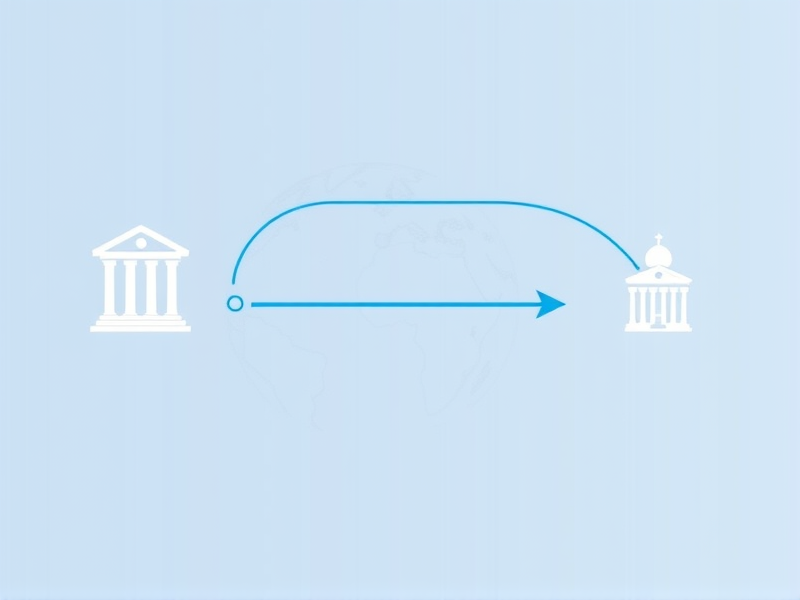

Under the proposed changes, institutions within the U.S. could leverage FedNow to send funds to a correspondent bank that would handle the international portion of transactions. This modification aims to broaden the scope and applicability of FedNow, building on its existing growth.

Hugh Thomas, Lead Commercial and Enterprise Analyst at Javelin Strategy & Research, commented, “A shift to cross-border payments via FedNow represents a logical progression in U.S. real-time payments systems. Aligning with the domestic speed seen in regions like the EU and UK further solidifies its position as a viable option for instant transactions.” Thomas noted that integrating ISO 20022 standards could enhance cross-border payment possibilities, though implementation challenges persist.

Border Limits

While the domestic segment of cross-border payments would benefit from real-time settlement through FedNow, international transfers beyond U.S. borders would revert to traditional correspondent banking processes, subjecting transactions to fees, currency conversions, delays, and reduced transparency.

The complexities associated with correspondent banking continue to pose significant challenges in modernizing global payment systems, as evidenced by the Group of 20 countries’ efforts to improve cross-border transactions through established roadmaps. However, legacy infrastructure and international coordination issues have impeded meaningful progress in this area.

Challenges and Alternatives

Addressing these obstacles may necessitate substantial changes to the cross-border payments landscape, potentially involving new payment rails such as stablecoins or global networks operated by Visa and Mastercard. The SWIFT messaging system is also advancing a framework for retail cross-border payments, but even with this progress, FedNow would still operate in an increasingly fragmented and complex global environment.

The Federal Reserve will carefully consider public feedback before deciding to proceed with expanding FedNow’s capabilities, weighing the potential benefits against ongoing challenges.